Tuck-in and bolt-on M&A is rarely revolutionary

My thoughts on Workday and HiredScore and some M&A advice for users.

It seems my writing mojo has returned. Here I dabble at my old analyst job. This post is in two bits, one about the Workday / HiredScore deal, the other a re-posting of my advice to users when vendors do the acquisition dance. And as usual, a musical treat at the end.

Part 1: Last week Workday acquired HiredScore

I have no inside knowledge of the deal or its terms. I’ll keep my valuation guesses to myself for now.

Josh Bersin’s take here. He calls it a potential shake up.

Kyle Lagunas called the Workday/HiredScore deal “biggest news since Oracle announced its acquisition of Taleo.”

I’m considerably less exuberant.

I’m not convinced this will shake up the market, it is a smart bolt-on (and eventually tuck-in) of a reasonably successful niche candidate matching / selection tool with an emerging AI competence. Workday could have bought one of half a dozen vendors doing similar stuff. It is a sensible, likely opportunistic move by Workday, but it is about as far from revolutionary as you can get.

It bolsters Workday’s recruitment product, which needs bolstering, but it doesn’t meaningfully shift the balance in the broader enterprise HR Tech battle with the likes of SAP, Oracle, Ceridian, UKG etc. I can’t see anyone replacing an incumbent ERP or core HCM because of this deal. It may make life a little harder for Workday’s erstwhile recruitment tech partners though.

A bit of history and a business model shift

Less than 10 years ago, Workday was all about the Power of One. It argued that to win, you needed a single, unified platform, with a carefully crafted, a priori data model and single consistent UX.

“At Workday, we have one version of software, one customer community, and one codeline. Together, these things empower us all in ways that weren’t possible in the legacy software industry.”

The sales model was based on one big deal and then the promise of SaaS would mean innovation and compelling new features will flow over time.

This model is great when most of your revenue is coming from new deals. When you are the insurgent challenging the incumbent it works brilliantly. Your pricing and product are clean and transparent. I call this the buffet all you can eat pricing. SAP and Oracle were on the backfoot because they were managing a series of acquisitions. Their technology story was complex, as were their price lists. Workday offered an innovative product with a really simple pricing model. This was a massive success. Chapeau.

Insurgent to incumbent

Workday is now an incumbent. It makes more money from existing customers than expanding to net new ones. It is no longer the disruptor, it is part of the status quo. The problem with the “buffet” business model is that it is tough to convince existing customers to pay you for new smaller feature sets when they bought the all you can eat menu promise a few years before.

That pricing model discourages significant feature innovation on the core product, because customers believe they are entitled to enhancements as part of the original buffet deal, so it is tough to charge more. Incremental feature builds don’t have the ROI.

Workday needs to continue to improve its net revenue retention, (ie upsell to existing customers). Workday has had massive success with the Power of One. It has built an impressive customer base and a strong sales machine. The sales kit bag has space for more goodies.

The easiest way to add an extra to the buffet price list is to do an acquisition. It did this with Peakon, VNDLY, Adaptive Insights and more. Once companies have built an M&A machine, it is hard to switch it off, so I expect to see more going forward.

Technology wise, Workday’s core platform has become less of an advantage over time as it gets bigger, more unwieldy and just older. Messing with that initial data model is like scrapping sauce off the spaghetti. Buying ends up being easier than building. Conway’s law rules too.

Workday will build out its financial products, and it needs renovate its increasingly venerable technology stack. It will acquire niche products, especially in HCM, as it has an enviable customer base to sell to.

This is not revolutionary, it is merely repeating the model that SAP, Oracle and others followed before. A decade ago, If SAP or Oracle had made this sort of acquisition Workday would have derided it as Frankensoft. But today Workday is a different company from what it was then. These sort of of acquisitions become routine for large incumbents. Some do it better than others. Incumbents are judged as much by their acquisition skills and post merger efforts as they are by core R&D capabilities. Exhibit A being Salesforce.

Partner disruption

In the times of Power of One, niche vendors found Workday hard to partner with. It wasn’t open with APIs, and had relatively limited joint GTM etc. This has begun to shift, with more open architecture, and a more partner-aware attitude. As SAP and Oracle have known for years, partners can be monetized, and Workday is likely to follow the same path.

However, Workday has developed an awkward habit of opening a space for partnering and then building or acquiring suddenly. If it is to strengthen its nascent partner ecosystem, it will need to balance its acquisition appetite with a more coherent partnering approach.

About AI

All the incumbent vendors are strengthening their AI efforts, and acquisitions are an important component of that. With this deal Workday has added more AI engineers and some useful functionality, and a new set of articulate evangelists. There will be more of these sort of incremental acquisitions.

The AI efforts of the HCM players have been merely augmentative to date, rather than disruptive or radical. I’d argue that ServiceNow is doing more in deep AI and articulating it better than the usual HR and ERP suspects (check their share price), but that is for another day.

Perhaps Workday will do a bold acquisition soon, but this isn’t that. It’s prudent but not bold.

M&A is back

Valuations for companies like HiredScore today are probably 40% or more down on where they would have been a year or two ago. Series B and C and later stage funding is still tight, and the IPO window is still shut. But share prices in the public markets for companies like SAP, Workday etc have recovered nicely, and they all have lots of cash. There will be plenty of action this year.

================

Part 2: Advice for HR leaders

I lifted this from an old post I wrote about M&A implications for HR departments. I wrote this when Workday acquired Peakon a few years ago. I reckon it holds up rather well.

Prepare yourself for the M&A possibility

At least once a year, HR leaders should list out all their niche vendors, and estimate the likelihood that they will be acquired or not in the next 12 months. While you will probably guess wrongly, the effort of prediction will mean you prepare yourself for the possibility.

Remember, at some point most of the niche vendors you use will be acquired, or have some sort of significant financial event (good or bad). Heck, even your suite vendor might get acquired.

When an acquisition is announced, here’s what you should do first:

1. Understand the situation within a few days of the acquisition:

Who is making the acquisition, and why?

Is it being acquired by a vendor that you work with already, or is it from a different ecosystem?

Is being acquired for the technology, or is it being acquired for the customer base and revenue?

What is the track record of the acquiring vendor with other acquisitions?

What is the product overlap with the acquiring vendor’s portfolio?

Where is the acquirer headquartered?

2. Assemble key information (you should have this at your fingertips because you run a tight tech asset inventory):

What business processes do you run on the acquired vendors tech?

What licenses or subscriptions do you have? When do they come up for renewal?

What is the current committed roadmap?

How to react to the acquisition as an HR leader?

1. Your niche vendor has been acquired by a vendor you use already

In this case, you are in a strong position. Take advantage of the period between announcement and acquisition to negotiate any renewals etc. Usually acquired products become more expensive once acquired by the suite vendors.

Here’s what you could do right away:

Establish why they have done the deal.

You are unlikely to discover details of the integration plans because of the quiet period until the deal formally closes, but start asking anyway. Ask to be in the early feedback loop

Is a tuck-in or bolt on play? (It is important to know the difference).

Identify key leaders from the acquired company that may be at risk of heading to the beach

Make sure you review your contracts, especially the data protection provisions, as a change of ownership is likely to have significant impact on risk, data controller/processor rules etc.

Use acquisition disruption to maximise your discounts.

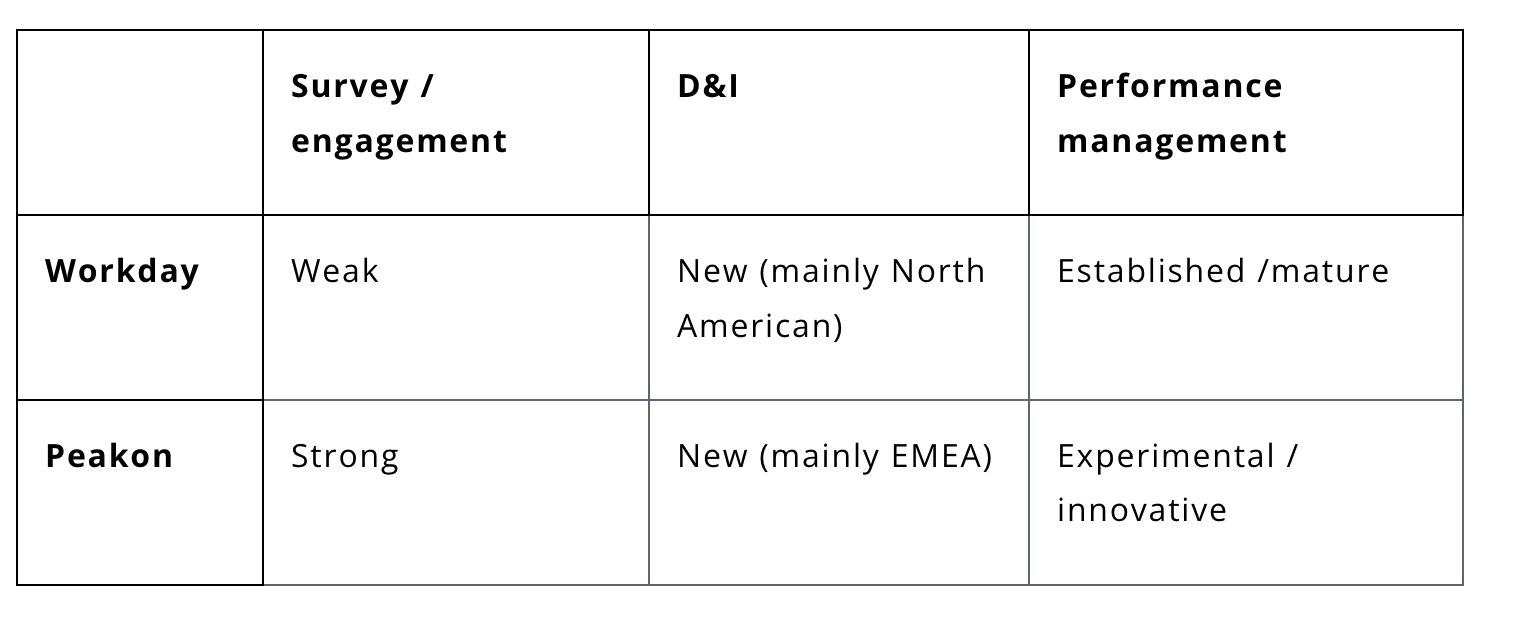

Understand product overlaps, and don’t always assume that the acquired products edge features will survive. Develop a product matrix. Here’s an example

Workday buys Peakon.

It is likely that both roadmaps will be disrupted. Timings are going to going to be toast, as the integration process will slow things down. Don’t bet on the the pre-acquisition roadmap. But all in all you are in a good place.

2. Your niche vendor has been acquired by a suite vendor you don’t use

In that case, you might have a problem. In the short term don’t panic, but the longer term attention won’t be on your needs, or on integration with your key vendor.

Here’s what you could do right away:

Lock in any pricing you have, as post acquisition, prices almost always go up.

Make sure you are good from GDPR perspective, because a change of ownership is a big deal, especially if it is an EU vendor being acquired by a US one

Start to assess your competitive options.

Use this as lever to beat up your suite vendor.

If integration isn’t that important and the application runs well standalone, then you don’t need to rush to replace it (there are still a lot of SuccessFactors performance management and learning customers running on top of non-SAP core HR systems, for instance).

Conclusion

In both cases, look at past track record of the suite HRTech vendor. How did the suite vendor manage its last acquisition? Check with other companies. Have a look in Linkedin and see who is still there a few years later.

With any acquisition there will be changes. The changes in the product teams will take time to have an impact on the product, but support and sales often have high turnover post acquisition as people may suddenly have stock options vest, or don’t fancy working with the big co. Don’t assume your friendly niche account manager will be there forever.

Always be expecting your cool niche vendors to be acquired. It is where we are in the cycle. Plan for it, and you will be so much better off than those who don’t.

And finally

For those that stayed til the end, here’s a musical treat. Phoebe Bridgers and Arlo Parks performing Radiohead’s Fake Plastic Trees. A brilliant collaboration.

Important and helpful advice. I found this thread similarly informative for those on the vendor side - https://twitter.com/thatguybg/status/1751978753712939391?s=46

Can't click fast enough on the TO e-mails when they land in my mailbox